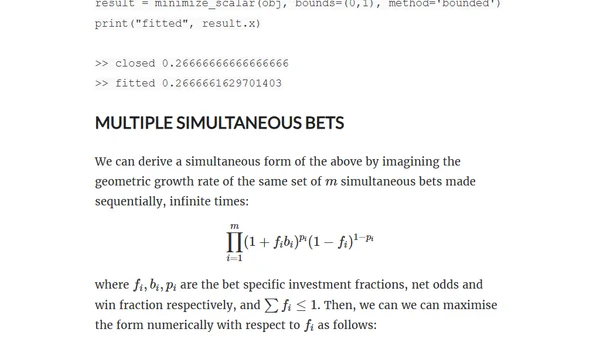

Kelly fractions for independent simultaneous bets

Read OriginalThis technical article details the Kelly criterion for optimal bet sizing in sequential binary bets, including its mathematical derivation. It then extends the concept to handle multiple independent bets placed simultaneously, formulating the optimization problem and providing a Python implementation using SciPy to calculate the optimal investment fractions across all bets.

Comments

No comments yet

Be the first to share your thoughts!

Browser Extension

Get instant access to AllDevBlogs from your browser

Top of the Week

1

Limit token usage in Microsoft Agent Framework

Jesse Liberty

•

1 votes

2

How to Roll Back AI Agents: Incident Response, Circuit Breakers, and Recovery Patterns

Paul Bryant

•

1 votes

3

Avoiding Reasoning Model Failures with Microsoft Foundry

Luke Murray

•

1 votes

4

When Your AI Agent Lies: Silent LLM Fallbacks

Luke Murray

•

1 votes

5

Adding a custom MCP server to Claude and ChatGPT

Simon Willison

•

1 votes

6

Testing AI prompts and comparing models with promptfoo

Tim Deschryver

•

1 votes

7

Superlogical

Mitchell Hashimoto

•

1 votes